(2)")

In 2024, the Mageska Fund recorded a return net of fees of 16.17% for Series F and 16.93% for Series J, compared with a benchmark return of 19.26%. Nevertheless, the last five months of the year enabled the Fund to post a positive relative performance, thanks to an appropriate strategic positioning in a context marked by the U.S. presidential election and varied asset class trends.

The concentration of market returns in the largest capitalizations of the index in 2024 posed a significant challenge to outperforming the benchmark. However, the Fund’s strategy, based on prudent, diversified management, enabled it to generate competitive results while reducing risk.

We continued to optimize our investment models and operational processes, which helped strengthen relative performance during the year. The Fund holds an average of 20-22 positions in highly liquid U.S.-based exchange-traded funds (ETFs). Through the active use of passive instruments, we aim to generate positive alpha relative to our benchmark (60/40), while significantly reducing asset-specific risk.

In 2024, the Fund incorporated Bitcoin as a new asset class, offering increased diversification and return opportunities in a balanced portfolio. This approach reflects our commitment to innovation and adapting our strategies to market developments.

Back to 2024

While everyone was expecting a recession at the start of 2024, it didn’t materialize, despite one of the most aggressive rate hike cycles of recent decades. The resilience of the US economy, particularly in the consumer and employment sectors, was proof of this throughout the year. Financial markets were anticipating that the Federal Reserve would begin a cycle of rate easing as soon as inflation began to fall back to levels deemed more “normal”. However, this easing only materialized in September, the Federal Reserve having since cut rates by some 100 basis points.

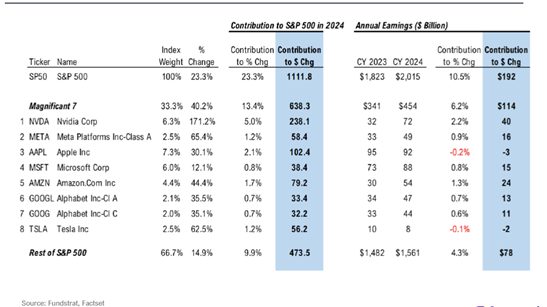

Magnificent Seven

For the second year running, the Magnificent Seven outperformed the S&P 500, accounting for 40.2% of the year’s total gains. Without their contribution, the S&P 500 would have returned a solid 14.9%, outperforming the majority of global equity markets.

Since October, the slowdown in inflation has raised questions. Will we see a return to the upward trend?

At the time of writing, some investors, and even members of the Federal Open Market Committee (FOMC), are concerned that the pricing policies announced by the new administration could rekindle inflationary pressures. The bond market will offer clues to this development, as discussed below.

Another significant story of 2024 was the rise of Bitcoin, surpassing the $100,000 threshold for the first time. With the advent of Bitcoin ETFs, we conducted extensive research and rigorous testing to integrate this asset class into our strategies. At the end of the year, the Mageska Fund held a small allocation in Bitcoin via the GBTC ETF.

The US presidential election also marked 2024 with its significant impact on the markets. As early as September, the market began to discount a possible victory for Donald Trump. We saw notable movements in sectors and asset classes such as financials, small caps, Bitcoin, the US dollar and Tesla (TSLA). Optimism followed his victory, but it remains to be seen whether it will be sustained in the long term.

And now, 2025

The coming year promises to be full of uncertainty. We anticipate a rise in volatility across asset classes, a dynamic favorable to the type of strategy we apply in the Mageska Fund. The ability to detect trends and filter out noise is key to effectively navigating the next four years of Trump’s second term.

POLITICAL AND MACROECONOMIC FACTORS

HIGHER FOR LONGER : A NEW ERA FOR INTEREST RATES

As we enter 2025, the dominant theme in the global economic landscape is Higher for Longer, reflecting high interest rates maintained over an extended period. Although the Federal Reserve initiated a rate-cutting cycle last September, long-term interest rates continue to climb, suggesting a fundamental shift in market expectations and economic conditions.

WHAT DOES THE BOND MARKET TELL US?

The persistent rise in 10-year bond yields since the Federal Reserve’s first rate cut is a cause for concern. As the chart below from Apollo Asset Management shows, yields on US 10-year bonds have historically tended to fall after the start of an easing cycle, a pattern not mirrored this time around.

Currently at 4.70%, any rise above the 5% threshold could weigh on both the profit margins of S&P 500 companies and the multiple applied to their earnings (price/earnings ratio). Combined with the market’s current valuation, which is in the upper percentile relative to the S&P 500’s history, the margin for error is slim. In the long term, the evolution of 10-year bond yields will be a key indicator of the economic and political orientations of the new US administration.

THE WEIGHT OF PUBLIC DEBT

The imminent renewal of almost $7,000 billion in US government debt is adding significant pressure to interest rates. Investors, demanding higher yields to absorb such a large volume of debt, are contributing to higher borrowing costs for the government. This dynamic is likely to further increase budget deficits in the years ahead.

PRESIDENT TRUMP’S ROLE

Against this backdrop, the Trump administration’s policies add economic unpredictability. At a recent press conference, the president-designate expressed dissatisfaction with high interest rates, while signaling his intention to weaken certain economic levers. Although his direct influence on monetary policy is limited, certain initiatives could have considerable repercussions:

- Aggressive trade tariffs: The introduction of new import tariffs is likely to intensify inflationary pressures and disrupt supply chains.

- Fiscal austerity: Measures such as DOGE (Deficit Optimization and Government Efficiency) could slow the economy by reducing public spending.

- Migration control: Tighter migration policies could exacerbate labor scarcity, putting upward pressure on wages and fuelling inflation.

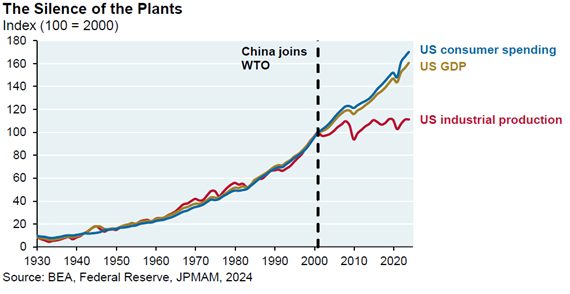

What’s more, the new Trump administration is committed to countering some of the consequences of China’s entry into the World Trade Organization, such as the stagnation of US industrial production, illustrated in the chart below.

The priorities outlined above, combined with the administration’s other commitments, including deregulation in several sectors, tax cuts, reduced government spending, promotion of cryptocurrencies, support for the oil and gas sector, and advances in artificial intelligence, could generate a complex and unprecedented set of economic and financial results.

MAGESKA’S PHILOSOPHY FOR NAVIGATING THESE UNCERTAIN TIMES:

FINANCIAL ASSET PRICE TRENDS

In the financial markets, one is generally not rewarded for dogmatic predictions about the future, but rather for the ability to generate profits.

At Mageska, we place great importance on price trends and the clues the market offers us. As price action evolves, so do we.

Our systematic, quantitative approach enables us to rigorously analyze market trends and identify relevant opportunities. Thanks to this discipline and our in-depth expertise, we adjust our portfolios in a thoughtful and adaptable way, in order to navigate effectively in an ever-changing environment.

Once again, those hoping for certainty or a crystal ball prediction will be disappointed, because that’s how the markets work. Uncertainty is at the heart of the game!

NEW PARTNERSHIP IN 2025 – NYMBUS CAPITAL INC.

In our ongoing quest to improve our investment processes and management tools, we are proud to announce a targeted partnership with Nymbus Capital, a Montreal-based asset management firm renowned for its avant-garde strategies and rigorous risk management.

Under this agreement, Mageska Capital entrusts Nymbus Capital with the management of a specific portion of the Mageska Fund to implement a portable alpha strategy.

This partnership will bring recognized expertise in uncorrelated, low-volatility strategies, enhancing the Mageska Fund’s return potential while reducing its overall correlation with its benchmark. We look forward to seeing the combined results of these strategies in 2025.

We would like to thank you for your trust and support, two essential pillars in ensuring the long-term success of a new firm like Mageska Capital. Please don’t hesitate to contact us with any questions or to discuss our strategies and approach.

Happy 2025!

Roberto Marrocco, CFA

Chief of investments and operations